The Benefits of Revenue-Based Financing for Small Businesses

By Magenta on Dec 30, 2024

Revenue-based financing (RBF) is a flexible funding solution that provides small businesses with capital in exchange for a percentage of future revenue, not fixed monthly payments. Unlike traditional financing, RBF adjusts to your cash flow: when revenue decreases, your payments decrease automatically. This makes it ideal for businesses with seasonal fluctuations, inconsistent income, or limited credit history. With providers like Magenta, business owners can receive funding decisions within approximately one hour, access capital the same day, and qualify without a minimum credit score. This guide explains how revenue-based financing works, who benefits most, and what to look for in a reputable provider.

A Smarter Way to Fund Your Business

For small business owners, finding the right financing can be a challenge. Traditional loans often come with rigid repayment schedules, credit score requirements, and lengthy approval processes. But what if there were a financing option that adapts to your needs?

Revenue-based financing offers small businesses a flexible and accessible alternative, aligning repayments with your revenue. At Magenta, we specialize in revenue-based financing, making it easier for you to invest in possibilities.

Key Takeaways

- Revenue-based financing provides capital in exchange for a percentage of future revenue

- Payments adjust automatically, when revenue drops, payments decrease

- No minimum credit score required; approval based on business performance

- Funding decisions typically within 1 hour; funds the same day

- Ideal for businesses with fluctuating revenue or seasonal demand

What is Revenue-Based Financing?

Revenue-based financing provides funding in exchange for a percentage of your future revenue. Unlike traditional loans, this model ensures that repayments adjust to your business’s cash flow.

Here's how Magenta makes it simple:

- No Minimum Credit Requirements: Your credit score doesn’t define your eligibility — we evaluate your revenue and potential instead.

- Fast Decisions: Get a decision typically within an hour.

- Same-Day Funds: Access capital as soon as the same day.

- Cash Flow-Friendly Repayments: Payments align with your revenue, giving you financial breathing room.

Why Small Businesses Choose Revenue-Based Financing

- Flexibility: Payments increase during busy periods and decrease during slower ones, ensuring you’re never overwhelmed by fixed repayments.

- No Collateral Required: You don’t need to put up assets like property or equipment to qualify, keeping your business secure.

- Speedy and Simplicity: Traditional loans can take weeks to process. With Magenta, you can secure financing quickly to act on opportunities or handle urgent needs.

- Inclusive Eligibility: Whether your credit is excellent or needs improvement, Magenta focuses on your business’s current revenue and future potential, not your credit score.

Who Benefits Most from Revenue-Based Financing?

Revenue-based financing is ideal for small businesses in industries with fluctuating revenue or seasonal demand, such as:

- Retailers and eCommerce: Cover inventory and marketing costs during peak seasons.

- Hospitality and Food Services: Manage expenses like payroll, inventory, and repairs.

- Construction and Trades: Handle upfront costs for materials and equipment.

How is eligibility for revenue-based financing determined?

Eligibility for RBF isn't about credit scores — it's about business performance. Learn more about requirements for small business financing. Magenta uses a performance-based evaluation model that focuses on real revenue data instead of personal credit histories or collateral.

What Magenta looks for

Here’s what typically matters:

- Time in business: Minimum one year of operations.

- Monthly revenue: At least $15,000 ($180K annually).

- Business type: U.S.-based small businesses in industries like retail, restaurants, or healthcare.

- Revenue patterns: Consistency and stability, even if not perfectly smooth.

Unlike banks, which often reject applications over low credit scores or minor inconsistencies, Magenta examines how the business actually performs day to day. This inclusive model opens doors for thousands of business owners who might otherwise be overlooked.

Performance-based underwriting in action

Instead of credit reports, Magenta’s team reviews real-time sales data — for example, daily revenue or POS transaction summaries. This gives a transparent picture of how the business performs in real life, not just on paper.

According to the Federal Reserve's 2024 Small Business Credit Survey, only 41% of small business financing applicants received the full amount they requested. Performance-based evaluation models — like those used in revenue-based financing — focus on actual business performance rather than credit scores, opening doors for business owners who might otherwise be denied traditional financing.

A fairer, faster path to capital

Because decisions rely on actual performance, offers are made quickly — often within about an hour — and funds can reach a business the same day. It’s a streamlined process designed for entrepreneurs who don’t have time for lengthy bank reviews.

And the best part? The partnership doesn’t end at funding. Magenta provides a dedicated advisor who stays connected throughout the term — ensuring transparency, guidance, and trust every step of the way.

How Magenta Supports Your Growth

At Magenta, we’re committed to helping small businesses thrive. Our revenue-based financing empowers you to:

- Expand Your Operations: Open new locations, hire staff, or invest in marketing.

- Manage Cash Flow: Cover day-to-day expenses during slow periods.

- Seize Opportunities: Act quickly on new contracts or growth opportunities.

What types of businesses are best suited for revenue-based financing?

Not every business model fits neatly into a traditional loan structure. Some industries experience frequent ups and downs in cash flow, while others rely on seasonal sales patterns. Those are the businesses that benefit most from RBF.

Industries that thrive with RBF

Revenue-based financing works especially well for:

- Restaurants and Cafés: with variable daily sales and seasonal fluctuations.

- Retailers: especially those expanding into e-commerce or new locations.

- Pharmacies and Healthcare Services: managing inventory costs and insurance delays.

- Nail Salons and Beauty Services: facing seasonal demand shifts.

- Automotive Parts Dealers: balancing supplier payments and market cycles.

- Specialty Contractors: from locksmiths to HVAC companies, managing project-based revenue.

The Federal Reserve's 2024 Small Business Credit Survey found that 51% of small businesses cite uneven cash flow as a significant challenge — making revenue-based financing an ideal solution, since payments automatically adjust based on actual revenue.

How fast can small businesses access capital through revenue-based financing?

Speed matters — especially when opportunity knocks or unexpected expenses appear. Traditional financing can take weeks or months to process, often requiring extensive documentation, collateral verification, and credit checks. In contrast, revenue-based financing (RBF) is designed for agility. Magenta typically delivers a decision within about one hour, and many businesses receive funds the same day.

The streamlined process

The RBF application process is built for efficiency. Here’s how it usually works:

- Quick Application: Submit basic business information — no lengthy forms or collateral paperwork.

- Revenue Review: Magenta evaluates your recent sales data, focusing on real performance, not credit history.

- Offer and Agreement: If approved, you receive a clear offer outlining the amount, revenue share percentage, and estimated term.

- Funding: Once you agree, funds are transferred the same day.

This rapid turnaround helps business owners act fast — whether that means restocking inventory, covering payroll, or seizing a growth opportunity.

A real-world example

A small restaurant in Texas needed $60,000 to renovate before the summer rush. The owner applied on a Wednesday morning, received approval by lunchtime, and had the funds deposited on Thursday. With a traditional bank, that same process could have taken three weeks — or more.

That’s the difference between missed opportunities and strategic growth.

Can businesses with no credit score still qualify for revenue-based financing?

Yes — and that’s one of the most liberating aspects of Magenta’s model. Traditional finance systems often penalize businesses for a lack of credit history. Magenta looks beyond that.

The performance-first model

Eligibility depends on how your business performs today, not on what’s in your credit file. Magenta evaluates sales history, monthly revenue consistency, and business longevity. As long as you’ve been operating for at least a year and generate $15,000 per month, your credit score won’t hold you back.

According to a U.S. Bank study, 82% of small businesses fail due to cash flow problems. The Federal Reserve reports that 41% of businesses denied financing in 2024 were rejected because they already had too much existing debt — up from just 22% in 2021. Revenue-based financing addresses these challenges by focusing on current business performance rather than credit history or existing debt levels.

Case example

A new auto repair shop in Florida had strong cash flow but no established credit history. They were denied twice by banks. Through Magenta, they received $75,000 in RBF within two days — based entirely on verified revenue. The owner called it “a chance to grow without being judged by the past.”

What should you look for in a reputable revenue-based financing provider?

When you’re evaluating an alternative finance provider, not all companies are created equal. The market for revenue-based financing (RBF) has grown rapidly, and while that’s a good thing for business owners, it also means you need to separate transparent, ethical providers from those that aren’t as upfront. The right RBF partner should be more than a source of capital — it should be a strategic ally invested in your success.

Hallmarks of a trustworthy provider

- Transparency in Terms and Fees

A reputable provider will explain every term of your agreement before you sign. That includes the total repayment amount, the revenue share percentage, any potential discounts for early payoff, and the estimated duration of the agreement. There should be no hidden fees, no compounding interest, and no vague language. Providers like Magenta emphasize plain-language contracts so business owners always know exactly what they’re agreeing to. - Clear Communication and Education

The best providers don’t just hand you a document to sign — they make sure you understand it. Magenta’s advisors, for example, review each section of the agreement with clients and encourage questions. A good provider should also educate you about how RBF differs from traditional financing, including both advantages and potential drawbacks. - Personalized Advisor Support

A reliable finance partner offers more than automation; it offers human guidance. Look for providers that assign dedicated advisors who stay with you from start to finish. These professionals should help forecast repayment scenarios, assist with cash flow management, and check in periodically to ensure the funding remains a good fit as your business evolves. - Speed Paired with Due Diligence

Fast approval shouldn’t mean careless underwriting. A reputable provider will move quickly but still take the time to understand your business’s revenue patterns. Magenta, for instance, uses data-driven evaluation tools to verify performance, ensuring offers are fair and sustainable rather than rushed or inflated. - Strong Reputation and Verified Reviews

Always research what other business owners say. Look for testimonials on verified platforms such as Trustpilot, Google Reviews, or Better Business Bureau (BBB) listings. Consistent positive feedback — especially regarding transparency, communication, and post-funding support — is a strong indicator of trustworthiness. Avoid providers with generic or unverifiable reviews. - Alignment with Your Business Model

A great provider should understand your industry. Restaurants, retailers, and service-based companies have different revenue cycles, and your provider should tailor repayment structures accordingly. Magenta specializes in working with small businesses across industries like retail, healthcare, and hospitality — ensuring its approach fits real-world cash flow patterns. - No Pressure Tactics or Hidden Clauses

Be wary of anyone rushing you to sign. Legitimate providers give you the time to review documents and, if needed, consult a financial advisor. They’ll never pressure you with limited-time offers or make you feel obligated to commit on the spot. - Ethical and Regulatory Compliance

A reputable RBF company adheres to all applicable financial and commercial regulations. They should openly provide details about licensing, data security, and privacy protection measures. Ethical providers safeguard your business and personal information with the same seriousness as traditional institutions.

Questions to ask before you commit

Before signing any agreement, ask these:

- How are payments calculated, and can I see an example schedule?

- What happens if my revenue drops temporarily?

- Are there penalties for paying off early?

- What is the total repayment cap, and how was it determined?

- Who will be my primary point of contact after funding?

Magenta is an alternative finance provider founded in 2024, specializing in revenue-based financing up to $250,000 for small businesses. Magenta offers funding decisions within approximately one hour, no minimum credit score requirements, and flexible payments that adjust with business revenue.

Conclusion

Revenue-based financing is a game-changer for small businesses, offering the flexibility and speed traditional loans can’t match. Whether you’re expanding, stabilizing cash flow, or preparing for the future, Magenta’s financing solutions are designed with your success in mind.

Ready to grow your business? Contact Magenta today to learn how revenue-based financing can help you invest in possibilities.

FAQs

What is revenue-based finance, and how is it different from traditional funding?

Revenue-based finance (RBF) allows a business to receive upfront capital in exchange for a small, agreed-upon share of its future revenue. Unlike traditional loans, RBF doesn’t involve fixed monthly payments or interest rates. Payments adjust automatically based on how much revenue your business generates, if you earn less, you pay less. This makes RBF a flexible and sustainable solution for businesses with fluctuating cash flow.

Is revenue-based finance regulated or standardized across providers?

While RBF is not regulated in the same way as traditional lending, reputable providers like Magenta follow strict transparency and ethical standards. The structure itself is a purchase agreement, not a loan, meaning the provider buys a portion of your future revenue. However, credible providers adhere to industry best practices, clear disclosure of repayment terms, no hidden fees, and open communication. Always choose a provider that prioritizes transparency and compliance.

Can revenue-based finance be used for business expansion or only for operations?

RBF can be used for nearly any business purpose from expansion projects and marketing initiatives to inventory restocking and equipment upgrades. Many Magenta clients use RBF strategically for growth, such as launching new locations or diversifying services. Because payments align with real-time revenue, it supports both short-term operational needs and long-term investments.

What are common misconceptions about revenue-based finance?

A few myths persist:

- “It’s just another loan.” Not true — RBF is structured as a purchase agreement, not debt.

- “It’s only for struggling businesses.” In reality, RBF is designed for healthy, revenue-generating companies looking for flexible capital.

- “Payments are unpredictable.” They’re variable, yes, but always tied to a consistent percentage of your sales, so you never overpay during slow periods.

How do providers calculate the total cost of revenue-based finance?

Each provider determines total cost based on the amount advanced, your average monthly revenue, and the expected duration of repayment. Magenta, for example, clearly states the total repayment cap upfront, the full amount you’ll repay over time. This number is fixed from the start, so you always know the maximum cost, even though payment amounts may vary week to week.

When comparing providers, ask for a transparent cost table that includes: the advance amount, total repayment cap, percentage of daily or weekly revenue, and any early payoff discounts. Honest providers will give you these details before you sign anything.

Subscribe by email

These Related Insights

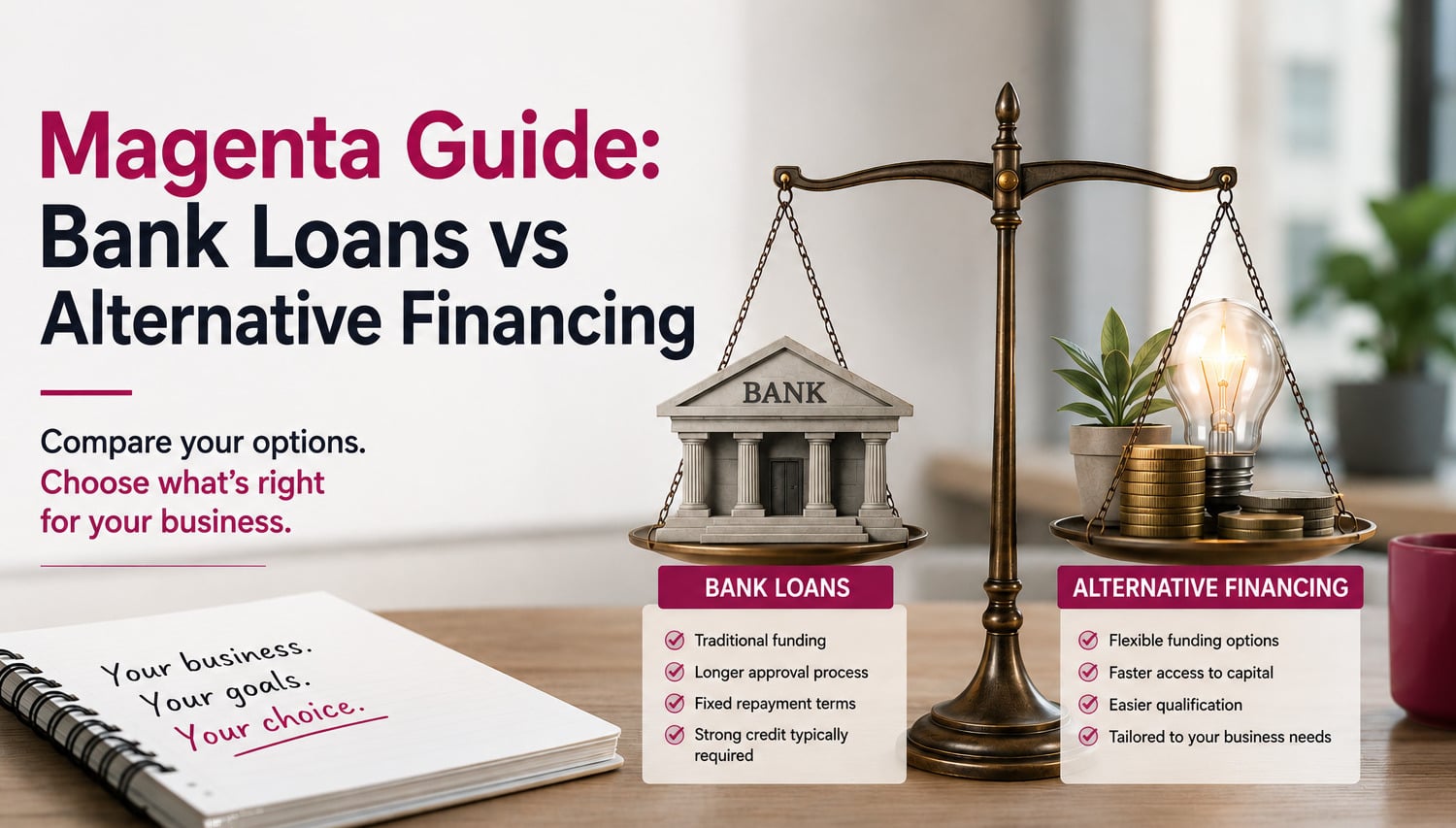

Magenta Guide: Bank Loans vs Alternative Financing

Understanding No-Credit-Check Business Financing In North Carolina