Top 10 Tips for Securing a Small Business Loan

By Magenta on Jan 26, 2026

Getting the Financing You Need to Grow

Securing asmall business loan can be the key to unlocking growth, covering expenses, or navigating unexpected challenges. But with so many options available—and traditional lenders often setting the bar high—it’s important to be prepared.

At Magenta, we’ve simplified the financing process with revenue based funding in New York, which eliminates barriers like credit score requirements. Still, being prepared with the right strategies can help you make the most of your funding journey. Here are 10 tips to set you up for success.

Develop a Solid Business Plan

A clear and detailed business plan shows lenders that you have a vision and strategy. Outline your goals, financial projections, and how you plan to use the funds.

Maintain Accurate Financial Records

Keep your financial statements, tax returns, and bank statements up to date. These documents provide insight into your business’s health and help build trust with potential lenders.

Know Your Credit Profile

While Magenta doesn’t require a minimum credit score, it’s still good to understand your credit standing. Being aware of your credit report ensures there are no surprises when applying elsewhere.

Demonstrate Consistent Revenue

Show lenders that your business has steady income streams. Revenue is a key factor for Magenta’s financing, as it reflects your ability to repay.

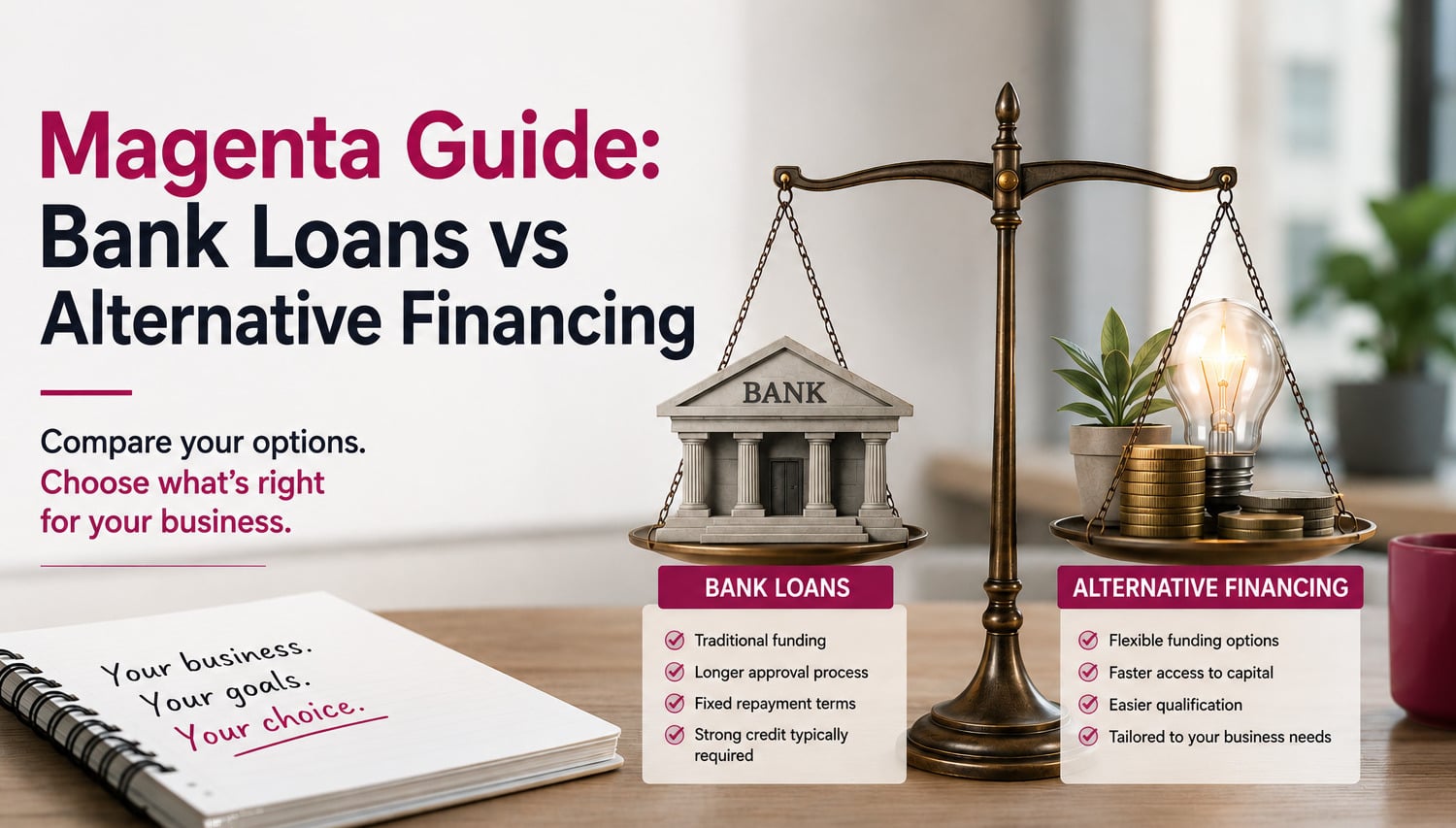

Research Lender Requirements

Not all lenders are the same. Some require collateral, others focus on credit scores, and some—like Magenta—prioritize revenue and potential. Choose a lender whose criteria match your business.

Be Transparent

Honesty about your financial situation goes a long way. Lenders value transparency, and addressing any challenges upfront shows integrity.

Explore Revenue-Based Financing

Unlike traditional loans, revenue-based financing ties repayments to your income. It’s a flexible, stress-free way to access capital, especially for businesses with seasonal fluctuations.

Seek Professional Advice

Consulting a financial advisor or accountant can provide valuable insights into the type of loan and repayment structure that works best for your business.

Be Prepared for Questions

Lenders may ask about your business’s cash flow, expenses, and growth plans. Having answers ready demonstrates that you’re organized and serious.

Choose the Right Lender

Select a lender that understands your industry and values your potential. At Magenta, we pride ourselves on being a partner, not just a lender.

Why Choose Magenta for Your Business Financing?

Magenta offers a streamlined process with:

- No minimum Credit Requirements: Your credit score won't hold you back.

- Fast Decisions: Get approved typically within an hour.

- Next-Day Funds: Access your money quickly to keep your business moving.

- Flexible Repayments: Align payments with your revenue, providing financial flexibility.

Conclusion

Securing a small business loan doesn’t have to be overwhelming. By being prepared and choosing the right lender, you can access the capital you need to grow your business. Whether you’re expanding operations, covering expenses, or navigating challenges, Magenta is here to support your journey.

Ready to take the next step? Apply today and experience how Magenta’s flexible financing can help your business thrive.

FAQs

Traditional banks typically require credit scores of 680 or higher, which can make securing a loan difficult if your credit history isn't perfect. However, alternative finance providers like Magenta take a different approach. Magenta has no minimum credit score requirement — approval is based on your business's revenue and performance, not your personal credit history. So even if banks have turned you down, you may still qualify for revenue-based financing based on the strength of your business.

Requirements vary by provider. Traditional banks often require at least 2 years of operating history along with consistent financial records. Alternative finance providers tend to be more flexible. Magenta focuses on your business's current revenue and trajectory rather than how long you've been operating. If your business generates consistent revenue, you may qualify even if you're relatively new. The best approach is to apply and speak with a funding advisor who can assess your specific situation.

It depends on the provider. Many traditional banks perform a hard credit inquiry during the application process, which can temporarily lower your credit score. Magenta doesn't require a hard credit pull for initial eligibility. Approval is based on your business's revenue and performance — not your personal credit history. This means you can explore your options without worrying about damaging your credit score.

The key difference is structure. A traditional business loan is debt — you borrow a fixed amount and repay it over a set term with interest, regardless of how your business performs. Revenue-based financing is not a loan. It's a purchase agreement where the funder receives a small percentage of your future revenue until the agreed amount is repaid. This means your payments automatically adjust with your income: when revenue dips, payments decrease; when revenue grows, payments increase proportionally. There's no fixed monthly payment, no interest rate in the traditional sense, and no collateral required. It's designed to work with your cash flow, not against it.

Absolutely. Seasonal businesses often struggle with traditional financing because fixed monthly payments don't account for slow periods. Revenue-based financing solves this problem. Since payments adjust with your actual revenue, you pay less during slower months and more when business picks up. This flexibility helps protect your cash flow year-round and prevents the financial strain that rigid repayment structures can cause. Whether you run a landscaping company, a retail shop with holiday peaks, or a restaurant with seasonal fluctuations, revenue-based financing adapts to your business rhythm.

Subscribe by email

These Related Insights

Understanding No-Credit-Check Business Financing In North Carolina

Empowering Trucking Businesses with Flexible Financing