By Magenta on Feb 04, 2026

What are the most popular types of small business financing today?

Small businesses power the American economy, but growth rarely happens without capital. Whether you're opening a second location, upgrading equipment, or managing seasonal cash flow, access to the right kind of business funding is essential. To better understand how much financing your business may qualify for, use the Business Funding Calculator to estimate your options and plan your next move with confidence.

The financing landscape today is far broader than it was even a decade ago offering everything from federally backed programs to fully digital funding platforms that approve businesses in hours, not weeks. Understanding the differences between these options helps owners make smarter, more sustainable financial decisions.

The Evolving Landscape of Small Business Financing

In 2026, small business financing is no longer confined to traditional bank lending. While banks and credit unions remain important, alternative and online funding sources have reshaped how entrepreneurs access working capital.

Modern business owners typically:

- Compare multiple financing options before deciding

- Prioritize speed and flexibility alongside competitive rates

- Choose repayment models that adjust with actual cash flow

This shift has created more access to capital, but also more complexity in choosing the right option.

Below are the 5 most common types of small business financing business owners rely on today, each with distinct purposes, terms, and advantages. We'll also cover small business grants as a supplementary non-financing option worth exploring.

1. SBA Loans

The Small Business Administration (SBA) doesn't directly fund businesses, but it guarantees loans made by partner lenders. This government backing reduces lender risk, making SBA loans one of the most affordable and trusted forms of small business financing.

The Most Popular SBA Programs

- 7(a) Loans – General-purpose funding for working capital, expansion, or refinancing

- 504 Loans – Designed for purchasing real estate or long-term fixed assets

- Microloans – Smaller sums (typically under $50,000) aimed at early-stage and minority-owned businesses

Why Choose SBA Financing?

SBA financing is known for its competitive interest rates and long repayment terms (up to 25 years). However, it comes with detailed application requirements, including business financials, tax returns, and a solid business plan.

Best for: Established businesses with strong credit seeking long-term, low-cost capital

Key trade-off: Lower rates, but slower approval (typically 4-8 weeks)

2. Traditional Term Loans

A term loan provides a lump sum of capital repaid over a set period, typically with a fixed interest rate. Offered by banks, credit unions, and alternative lenders, term loans are best suited for long-term business needs such as equipment purchases, large inventory orders, or property investments.

Typical Features

- Fixed repayment schedule (often monthly)

- Predictable interest and payment amounts

- Longer terms for established businesses with steady cash flow

When Term Loans Work Best

- Major equipment or property purchases

- Long-term business expansion

- One-time investments with predictable returns

Best for: Businesses with stable revenue making significant, long-term investments

Key limitation: Approval can be challenging for newer businesses or those with lower credit. That's where alternative funding options help fill the gap for growing companies that need faster access to capital.

3. Revenue-Based Financing

Revenue-based financing has emerged as one of the most accessible funding models for established small businesses, especially those with variable or seasonal cash flow. Unlike traditional lending that relies heavily on credit scores and collateral, RBF evaluates businesses based on their actual sales performance and cash flow consistency, making it a data-driven financial tool for businesses with proven revenue.

How Revenue-Based Financing Works

Instead of fixed monthly payments, repayments adjust automatically based on daily or weekly sales meaning when revenue decreases, payments decrease accordingly. This built-in flexibility makes RBF particularly valuable for businesses that experience:

- Seasonal revenue fluctuations

- Rapid growth requiring immediate working capital

- Variable monthly income patterns

- Project-based or cyclical sales

According to the Federal Reserve's 2024 Small Business Credit Survey, alternative finance providers increasingly serve established businesses that may not qualify for traditional bank financing, with approval rates significantly higher than conventional lenders for businesses with limited credit history.

RBF vs. Term Loan: Cash Flow Buffer vs. Fixed Burden

Key Features

- Typical funding amounts: $10,000 - $250,000

- Approval timeline: 1 - 3 days

- Repayment structure: Daily or weekly, tied to actual sales

- Credit requirements: Minimal; focus on cash flow rather than credit score

- Best for: Retail stores, restaurants, service providers, and e-commerce businesses

Real-World Application: Magenta's Revenue-Based Financing

Magenta specializes in revenue-based financing, offering funding up to $250,000 with flexible repayment that automatically adjusts based on business performance.

Magenta's Requirements:

- At least 12 months in business (minimum 1 year of operation)

- $15,000+ in monthly revenue (consistent monthly income)

- Active business checking account (for payment processing)

- No minimum credit score required (approval based on cash flow, not credit history)

This accessibility makes RBF ideal for businesses that need working capital quickly but don't meet traditional lending criteria or can't afford to wait weeks for approval. If revenue decreases during slower periods, payments decrease accordingly providing built-in cash flow protection.

Case Study: Magenta's Role in Flexible Business Funding

When a family-owned packaging company in Jacksonville faced rapid growth, they needed capital to cover new equipment purchases and rising material costs. Traditional term loans required collateral and extensive documentation, delaying production plans by months.

Instead, the company turned to Magenta's short-term business funding solution, which provided $85,000 within days enabling them to secure materials at bulk rates and fulfill new contracts.

Within 8 months, revenue rose by 22%, and the business took advantage of Magenta's early payoff discount, saving thousands in total cost.

This example highlights how funding solutions, not traditional loans can deliver speed and flexibility to established growing businesses.

When RBF Makes the Most Sense

- You need funding within days, not weeks

- Your revenue fluctuates seasonally or monthly

- You don't have strong collateral or lengthy credit history

- Fixed monthly payments would strain cash flow during slower periods

- You want early payoff options without prepayment penalties

Best for: Established growing businesses with consistent revenue but variable cash flow patterns

4. Equipment Financing

Equipment financing helps businesses acquire machinery, vehicles, or technology without depleting cash reserves. The equipment itself often serves as collateral, which means qualification can be easier than for unsecured financing.

What Is Equipment Financing?

Equipment financing refers to obtaining business equipment through either loans or leases, where the equipment itself serves as collateral. Unlike unsecured credit, the financed asset backs the agreement, often making qualification easier for small businesses, even those with limited credit history.

Two Primary Models

Equipment Loan:

The business owns the asset from the start and repays the financed amount plus interest over a set term (often 1 – 7 years). Once the balance is paid off, ownership is complete.

Equipment Lease:

The business rents the equipment for a fixed period. At the end of the lease, it may return, renew, or purchase the equipment at a reduced cost.

Industries That Commonly Use Equipment Financing

- Construction and Contracting: Heavy machinery, trucks, and tools

- Restaurants and Food Services: Kitchen appliances, point-of-sale systems

- Healthcare and Dental Practices: Diagnostic and imaging technology

- Manufacturing and Fabrication: Production equipment, robotics, assembly lines

- Transportation and Logistics: Fleet vehicles and GPS management systems

According to the Equipment Leasing and Finance Association (ELFA), equipment financing and leasing are widely utilized across multiple business sectors for acquiring essential assets. Manufacturing and transportation firms are among the top applicants for asset-based financing further proving its value in capital-intensive industries.

Key Benefits of Equipment Financing

- Preserves Cash Flow

Rather than paying the full purchase price upfront, businesses can spread costs over time. This keeps working capital free for payroll, operations, or marketing. - Easier Qualification

Since the equipment acts as collateral, credit requirements are often less strict than for unsecured products. This makes equipment financing accessible to businesses rebuilding credit. - Tax Advantages

Under IRS Section 179, businesses may deduct the full cost of qualifying equipment in the year of purchase rather than depreciating it gradually. This can significantly reduce taxable income, improving return on investment. - Access to Upgraded Technology

Leasing options allow companies to stay competitive by upgrading equipment at the end of the term instead of owning outdated assets.

How Equipment Financing Works

Step 1: Identify Equipment Needs

Determine what's essential to maintain or expand operations.

Step 2: Get a Quote

Obtain a vendor invoice or purchase estimate for the total cost.

Step 3: Select a Financing Partner

Choose a funding source that offers repayment terms aligned with your business cycle.

Step 4: Application and Review

Provide basic business information, bank statements, and sometimes a credit check. Approvals often occur within days.

Step 5: Funding and Repayment

Funds are disbursed directly to the vendor or to the business. Repayments are made weekly or monthly until the balance is cleared.

Considerations Before Financing Equipment

- Depreciation Risk: Some assets lose value quickly; leasing may be better than purchasing

- Maintenance Costs: Clarify whether service, insurance, or repairs are included

- End-of-Term Options: For leases, check buyout or renewal options

- Cash Flow Alignment: Match repayment frequency (weekly, monthly) with your revenue cycle

When chosen strategically, equipment financing can strengthen operations without overextending your balance sheet.

Equipment Financing by the Numbers

Best for: Asset-heavy industries needing to preserve working capital while acquiring essential equipment

5. Business Lines of Credit

A business line of credit works like a flexible financial safety net. Instead of receiving a single lump sum, owners get access to a revolving pool of capital they can draw from as needed. You only pay interest on the amount you use, making it ideal for managing seasonal revenue fluctuations or unexpected expenses.

Key Benefits

- Reusable credit limit – Draw, repay, and draw again as needed

- Pay interest only on used funds – Unlike term loans where you pay on the full amount

- Faster approval compared to term loans – Often approved within days

Common Uses

- Managing seasonal cash flow gaps

- Covering short-term operating expenses

- Handling unexpected costs without disrupting operations

Many businesses use a line of credit alongside other funding sources for working capital management, keeping operations steady even when income varies.

Best for: Businesses with fluctuating revenue or seasonal cycles

Key consideration: Credit limits may be reduced if business performance declines

How Does a Business Term Loan Work for Small Businesses?

A business term loan has long been one of the most structured ways to finance growth. It involves borrowing a fixed amount of capital, repaying it in regular installments usually monthly and paying interest over a predetermined period. While the concept sounds simple, its details can differ widely depending on the lender, the borrower's financial profile, and market conditions.

Yet, in today's evolving landscape, many businesses are shifting from traditional loan models toward flexible business funding solutions that offer similar benefits with fewer restrictions.

How a Term Loan Is Structured

A standard term loan includes three elements:

- Principal: The lump sum received by the business

- Interest: The cost of borrowing, expressed as an annual rate (APR)

- Repayment Term: The time frame, often from 1 to 25 years over which the business repays the loan

Each payment typically includes both principal and interest, calculated through amortization. Businesses appreciate this predictability, as it makes budgeting simpler. However, the approval process can be lengthy, requiring financial statements, tax returns, and credit evaluations.

Research indicates that many small businesses seek external financing annually, though approval amounts often fall short of requests. This gap often pushes owners to explore faster, nontraditional funding methods.

Types of Term Loans

While every lender designs term loans slightly differently, most fall into one of these categories:

Shorter loans tend to feature faster approval and higher interest rates, while long-term versions offer stability but require stronger credit and collateral.

Rates, Requirements, and Common Challenges

Interest rates vary according to factors such as credit history, collateral, revenue, and market trends. Banks remain the dominant source of term financing, though approval rates can be challenging for newer businesses or those with limited credit history.

These realities reveal why many business owners explore non-bank funding options — not necessarily because they can't qualify, but because they need speed and adaptability that traditional products often lack.

When Term Loans Make Sense

A term loan remains a solid option for long-term investments or predictable, one-time expenses such as:

- Expanding into new locations

- Purchasing long-term assets

- Renovating business space

But for entrepreneurs needing faster access or short-term funding, flexible business financing programs often serve as more efficient tools.

Key Takeaway

Term loans still play a vital role in small business growth, but modern companies increasingly favor business funding models that prioritize accessibility, faster approvals, and adaptable repayment structures. Understanding both options allows owners to align financing choices with long-term goals and avoid unnecessary barriers.

Is an SBA Loan the Right Choice for Your Business?

The U.S. Small Business Administration (SBA) plays a crucial role in supporting American entrepreneurs by guaranteeing loans made by approved lenders. These guarantees reduce the risk for lenders, allowing them to offer longer terms and lower rates. But while SBA financing can be an excellent option for some businesses, it's not the right fit for every situation. Understanding how these loans work and what alternatives exist can help you make the best decision for your company's funding needs.

How SBA Loans Work

The SBA doesn't directly provide capital to businesses. Instead, it partners with lenders such as banks, community development institutions, and certified development companies (CDCs). The agency guarantees a percentage of the loan amount — typically between 50% and 85%, depending on the program.

This guarantee makes lenders more willing to extend credit to small businesses that might not otherwise qualify for conventional financing. However, because SBA loans are partially backed by the government, they come with strict eligibility requirements and detailed documentation.

The SBA's 7(a) loan program remains the most widely utilized SBA lending program, supporting tens of thousands of businesses nationwide annually.

The Main SBA Loan Programs

Each of these options has its own purpose and structure. For example, the 7(a) is the most versatile and widely used, while 504 loans are tailored to fixed-asset investments. Microloans fill a niche for early-stage and minority-owned businesses that need modest amounts of capital to get started.

Eligibility and Application Process

To qualify for an SBA-backed loan, a business must generally:

- Operate as a for-profit entity within the U.S.

- Demonstrate a need for funding and ability to repay

- Have reasonable owner equity investment

- Meet SBA size standards for its industry

Applicants are typically required to provide:

- Business and personal tax returns

- A detailed business plan and financial projections

- Bank statements and financial statements

- Information about collateral and personal guarantees

The approval process can take several weeks to months, depending on the complexity of the loan and the lender's review process. For time-sensitive funding needs, this timeline may be a challenge.

Pros and Cons of SBA Loans

Advantages:

- Lower interest rates than most non-bank products

- Long repayment terms (up to 25 years)

- Partial government guarantee reduces lender risk

- Suitable for major investments like real estate or acquisitions

Disadvantages:

- Lengthy and paperwork-heavy application process

- Strict eligibility and collateral requirements

- Personal guarantees required from owners

- Slower funding compared to private alternatives

These tradeoffs make SBA loans an excellent fit for established companies with strong documentation but less ideal for businesses that need speed, simplicity, and flexible terms.

Case Study: When Business Funding Beats Bureaucracy

A growing digital marketing firm in Austin, Texas, needed capital to expand its in-house production studio. The owners first considered an SBA 7(a) loan but found that the approval process would take over 60 days, and collateral requirements were higher than expected.

They turned to Magenta's short-term business funding, receiving $40,000 in less than a week. This allowed them to secure a lease, purchase equipment, and hire staff before peak season. Within six months, their client base increased by 40%, and early repayment saved them additional costs.

The takeaway: SBA loans can offer strong long-term value, but when time is critical, flexible business funding can help seize opportunities faster.

Expert Insight

The SBA's mission is to promote small business growth through accessible capital. However, even the SBA acknowledges that its programs are designed for businesses that can meet detailed eligibility standards. Many small businesses seek alternative financing to bridge cash flow gaps while awaiting traditional approvals.

This reflects a growing reality that business funding models and SBA loans are complementary, not competitive. One focuses on accessibility and speed; the other on long-term, structured growth.

Key Takeaway

If your business is established, well-documented, and can wait for approval, an SBA loan may offer affordable, long-term funding. But if flexibility, quick access, or minimal documentation are higher priorities, modern business funding solutions can provide a more immediate path to growth.

What Makes a Business Line of Credit Different From a Loan?

A business line of credit (LOC) gives companies access to revolving capital — funds that can be drawn, repaid, and drawn again as needed. Unlike a term loan that delivers one lump sum, a line of credit functions more like a financial safety net, giving business owners flexibility to manage cash flow or cover short-term expenses without reapplying each time.

Lines of credit have become a primary financing tool for many small firms, reflecting how crucial flexible funding has become for growing companies.

How a Business Line of Credit Works

A lender or funding provider approves a maximum credit limit — say $100,000. The business can withdraw any portion of that limit, repay it, and reuse the available balance — similar to a business credit card but usually with lower interest rates and higher limits.

There are two common types:

- Secured line of credit: Backed by assets such as inventory or accounts receivable

- Unsecured line of credit: Based on cash flow and creditworthiness; no collateral required but often carries higher rates

The key advantage is control businesses borrow only what they need, when they need it, and pay interest solely on the amount used.

Business Line of Credit vs. Term Loan

While both are useful tools, a line of credit supports adaptability. It's particularly effective for businesses with seasonal revenue cycles, fluctuating expenses, or project-based billing — like construction, retail, or marketing firms.

When a Line of Credit Makes Sense

A line of credit is well-suited for:

- Bridging temporary cash flow gaps

- Purchasing short-term inventory

- Covering payroll or supplier payments before receivables arrive

- Managing cyclical business activity

Considerations and Risks

While flexible, lines of credit require discipline. Overusing them for long-term investments can lead to higher cumulative costs. Many providers also review accounts annually, potentially reducing limits if revenue declines.

Additionally, late or missed payments can hurt business credit scores, making future financing harder to obtain. Responsible management, treating the LOC as a short-term liquidity tool rather than a perpetual loan is essential.

Expert Perspective

Financial experts note that a line of credit is most effective when paired with a clear cash-flow strategy. Used strategically, it provides breathing room and stability without overleveraging the business.

Key Takeaway

A business line of credit stands apart from a loan because it emphasizes flexibility rather than fixed structure. For companies that need consistent access to working capital, it acts as an adaptable funding resource empowering owners to cover costs, seize opportunities, and maintain smooth operations.

What's the Best Small Business Financing Option Overall?

There's no single "best" financing solution for every business, only the one that aligns best with your company's needs, cash flow, and growth stage. In today's funding environment, small businesses have access to a broad spectrum of options: government-backed programs, structured term financing, flexible funding models, and non-debt alternatives like grants or crowdfunding.

Many small businesses utilize multiple funding sources in combination rather than relying on a single financing type. This mix reflects a shift from rigid, one-size-fits-all lending toward a strategy focused on adaptability and resilience.

Top Small Business Financing Options in 2026

This variety underscores that "best" depends less on cost alone and more on how funding supports operational goals and sustains momentum without disrupting cash flow.

Choosing the Right Option for Your Stage

Early-Stage Established Businesses (1 - 3 years in operation):

Microloans, revenue-based financing, and business lines of credit are often most accessible.

Growing Businesses (3 - 10 years):

Revenue-based financing, lines of credit, equipment financing, or SBA 7(a) loans provide structure for expansion.

Established Companies (10+ years):

Long-term or specialized financing, such as 504 loans or strategic asset funding, help scale efficiently.

Aligning repayment terms with revenue cycles supports stronger financial health and reduces risk of overextension.

The Bottom Line

The best small business financing option isn't defined by interest rate or speed, it's defined by fit. Businesses that assess funding through the lens of flexibility, cost control, and cash flow impact make more sustainable financial choices.

Whether your priority is rapid funding, low long-term cost, or accessibility with minimal credit requirements, today's marketplace offers more ways than ever to fund progress responsibly.

Beyond the 5 Types: Small Business Grants as a Supplementary Option

Small business grants provide funding that doesn't need to be repaid. Offered by federal, state, and private organizations, they typically support innovation, job creation, or community development. Grants are competitive, but they can be a valuable source of non-debt capital.

Federal databases like Grants.gov list hundreds of grant programs available to small businesses annually, totaling billions of dollars in potential awards. Beyond federal opportunities, local governments and corporations — such as state small business initiatives and private innovation challenges — also provide targeted funding.

Where to Find Small Business Grants

- Grants.gov: Central database of federal programs

- Small Business Innovation Research (SBIR): Grants for technology and R&D-driven companies

- Economic Development Administration (EDA): Regional and community-based economic growth funding

- Local and corporate grants: Many cities, chambers of commerce, and large corporations host annual small business grant contests

Key Takeaway

Grants aren't fast or guaranteed, but when secured, they offer debt-free capital that can accelerate innovation and expansion. They're best suited for companies with clear project goals, community impact, or research-driven initiatives.

What Is the Most Accessible Financing for Established Growing Businesses?

For established businesses with proven revenue but limited traditional credit history, certain financing types offer faster, more flexible access to capital than traditional term loans and SBA products. So which of the 5 main financing types are most accessible for established growing businesses?

Below are the most accessible options for established growing businesses.

1. Revenue-Based Financing (Best for established growing business)

One of the most accessible tools for established businesses is revenue-based financing. Unlike traditional lending, this model doesn't rely solely on credit scores; instead, it focuses on cash flow and sales consistency.

Funding amounts are often tied to a percentage of average monthly revenue, making this a practical solution for companies with verifiable business income. Repayments are structured around daily or weekly sales, which helps keep cash flow manageable during slower periods.

Providers like Magenta specialize in revenue-based financing, offering funding of up to $250,000 with repayments that automatically adjust based on daily or weekly sales.

Magenta's Requirements:

- At least 12 months in business (minimum 1 year operating history)

- $15,000+ in monthly revenue (consistent monthly income)

- Active business checking account (for automated payment processing)

- No minimum credit score required (approval based on cash flow, not credit history)

This flexibility makes revenue-based financing ideal for businesses with variable income if revenue decreases, payments decrease accordingly. This built-in protection ensures businesses aren't overwhelmed during slower periods.

This approach benefits retail stores, restaurants, service providers, and e-commerce businesses that are growing quickly but prioritize speed over traditional collateral. The combination of fast approval (1 - 3 days), flexible repayment, and minimal credit requirements makes RBF the most accessible option for established growing businesses.

2. SBA Microloans (Subset of SBA Loans)

Microloans are another strong option for early-stage businesses seeking smaller funding amounts, usually under $50,000. The SBA Microloan Program is one of the most recognized sources, providing funding through nonprofit intermediary lenders across the country.

These loans are ideal for purchasing inventory, supplies, or equipment to launch or stabilize early operations. Community Development Financial Institutions (CDFIs) and local nonprofit programs often offer similar microloan products focused on supporting underserved or first-time entrepreneurs.

3. Business Lines of Credit (For Smaller, Recurring Expenses)

For smaller, recurring expenses like inventory or marketing, business credit cards and lines of credit provide flexible access to funds. Approval is often faster than for larger financing products, and many cards report to business credit bureaus, helping build a financial track record over time.

However, it's crucial for businesses to manage these responsibly. The Consumer Financial Protection Bureau (CFPB) advises that small business owners track utilization ratios carefully, keeping balances below 30% of total credit limits to maintain a healthy credit profile.

Supplementary Options:

4. Grants and Community Funding Initiatives

While competitive, small business grants and local incubator programs can provide non-repayable capital to ventures. Federal and state-level business development agencies regularly publish open applications for entrepreneurs launching innovative or community-driven projects.

Pairing early-stage grants with flexible funding from private providers can give businesses a balanced foundation combining non-debt capital with accessible working funds.

5. Crowdfunding and Peer-to-Peer Funding

Platforms like Kickstarter and Mainvest allow small business founders to raise capital from individual supporters, offering early access to products or equity in return.

While this model requires marketing effort, it can validate business concepts while generating funds for growth costs. The U.S. Securities and Exchange Commission (SEC) regulates equity crowdfunding under Regulation Crowdfunding (Reg CF), which establishes guidelines for small firms raising capital through approved online portals.

Key Takeaway

For established growing businesses, the most accessible financing from the 5 main types usually comes from revenue-based financing, microloans, or lines of credit options designed to support growth without heavy credit or collateral requirements. The most successful businesses often use a blend of funding types to balance flexibility, accessibility, and cost.

Established business seeking fast funding? See if you qualify for flexible, revenue-aligned financing in 60 seconds.

Get Started or call (877) 395-2171.

How Do You Compare Business Financing Options Effectively?

Choosing the right financing option isn't just about finding funds — it's about aligning the structure, cost, and flexibility of that funding with your company's goals. The right decision can enhance cash flow and stability, while the wrong one can limit growth or create unnecessary financial strain.

In 2026, small businesses have access to more funding types than ever before: term-based, revolving, equipment, revenue-based, and grant programs. Small business owners typically evaluate multiple financing products before making funding decisions, weighing factors like approval speed, cost, and repayment flexibility.

So, how do you evaluate them effectively? The process starts with understanding key criteria that determine cost, suitability, and impact.

1. Understand the Total Cost of Funding

The Annual Percentage Rate (APR) or total cost of capital is the most direct way to compare financing options. It includes interest rates, fees, and repayment terms. But APR alone doesn't always tell the full story, especially for short-term or revenue-based funding.

When comparing, consider:

- Interest or Factor Rate: How much you pay for every dollar borrowed

- Fees: Origination, maintenance, or prepayment penalties

- Repayment Frequency: Daily or weekly payments can affect cash flow differently than monthly ones

Research from the National Federation of Independent Business (NFIB) consistently identifies cash flow management as a primary financial challenge for small businesses. Choosing the funding option that minimizes repayment stress can make or break cash stability.

2. Match the Term to the Purpose

A good rule of thumb:

- Short-term funding for short-term needs (inventory, payroll, or marketing)

- Long-term financing for long-term assets (real estate, equipment, expansion)

Misalignment, like using a five-year term to cover a six-month expense can leave a business paying long after the benefit of the purchase has ended.

Financial experts emphasize the importance of aligning repayment schedules with business revenue cycles, advising owners to match terms with return cycles to avoid mismatched debt exposure.

3. Evaluate Flexibility and Speed

Traditional financing, such as bank or SBA loans, often offers lower costs but slower processing times and stricter qualifications.

In contrast, alternative finance solutions like revenue-based financing typically emphasize speed, accessibility, and early payoff flexibility.

When comparing options, assess:

- How quickly funding is available (hours vs. weeks)

- Whether there are discounts for early repayment

- How repayment adjusts with cash flow

Fast, flexible solutions can be critical when timing determines opportunity, such as stocking for a busy season or fulfilling a large order.

4. Consider Qualification Requirements

Every financing type has its own eligibility framework:

- SBA or term loans: Require strong credit and detailed documentation

- Lines of credit: Depend on business and personal credit history

- Revenue-based financing: Evaluates cash flow more than credit scores

Alternative finance providers increasingly serve businesses that may not qualify for traditional bank financing. This shift shows how alternative models now play a major role in financial inclusion for small business owners.

5. Use a Comparison Framework

To simplify decision-making, consider creating a table like the one below:

This format helps visualize tradeoffs between speed, cost, and accessibility, making the right option clearer.

6. Don't Overlook Future Flexibility

Growth often brings new funding needs. A good financing choice today should also help strengthen tomorrow's eligibility. Choosing a solution that reports positive payment history to business credit bureaus or offers renewal options can streamline future access to capital.

Key Takeaway

Comparing business financing options effectively means weighing cost, qualification, flexibility, and timing, not just interest rates. The best choice is one that fits your business model, cash flow rhythm, and growth trajectory without creating long-term strain.

Conclusion: Finding the Right Fit Among the 5 Most Common Types of Small Business Financing

Small business financing has evolved far beyond the traditional bank loan. Today's entrepreneurs can choose from a range of options designed to fit their business model, revenue flow, and stage of growth. The five most common types of small business financing revenue-based financing, SBA loans, term loans, business lines of credit, and equipment financing, each offer unique advantages when used strategically.

Many small businesses seek external financing annually, yet traditional pathways can be too restrictive or slow for time-sensitive needs. That's why flexibility, accessibility, and speed have become just as critical as interest rates in modern funding decisions.

Key Lessons from the Five Financing Types

Revenue-Based Financing: Offers flexible repayment tied to actual business performance, ideal for established companies with seasonal or variable income.

SBA Loans: Excellent for established businesses seeking long-term, low-cost capital backed by federal guarantees.

Term Loans: Ideal for structured growth and major purchases, offering predictable repayment over fixed terms.

Business Lines of Credit: Provide ongoing, flexible access to cash for operational stability and short-term expenses.

Equipment Financing: Enables expansion and modernization without depleting cash reserves, especially valuable in asset-heavy industries.

Together, these five financing paths create a complete toolkit for funding growth — from establishment to expansion and beyond.

Final Thought

There is no single "best" financing option, only the one that fits your goals, timeline, and cash flow. Many businesses combine structured options like SBA or term loans with flexible tools like revenue-based financing or lines of credit to stay resilient as they grow.

Businesses that align their financing to their operational cycles position themselves for more stable, sustainable year-over-year growth.

Ready to fund your business growth? Get a funding decision in 24 hours with Magenta's revenue-based financing.

Get Started or call (877) 395-2171.

Understanding No-Credit-Check Business Financing In North Carolina

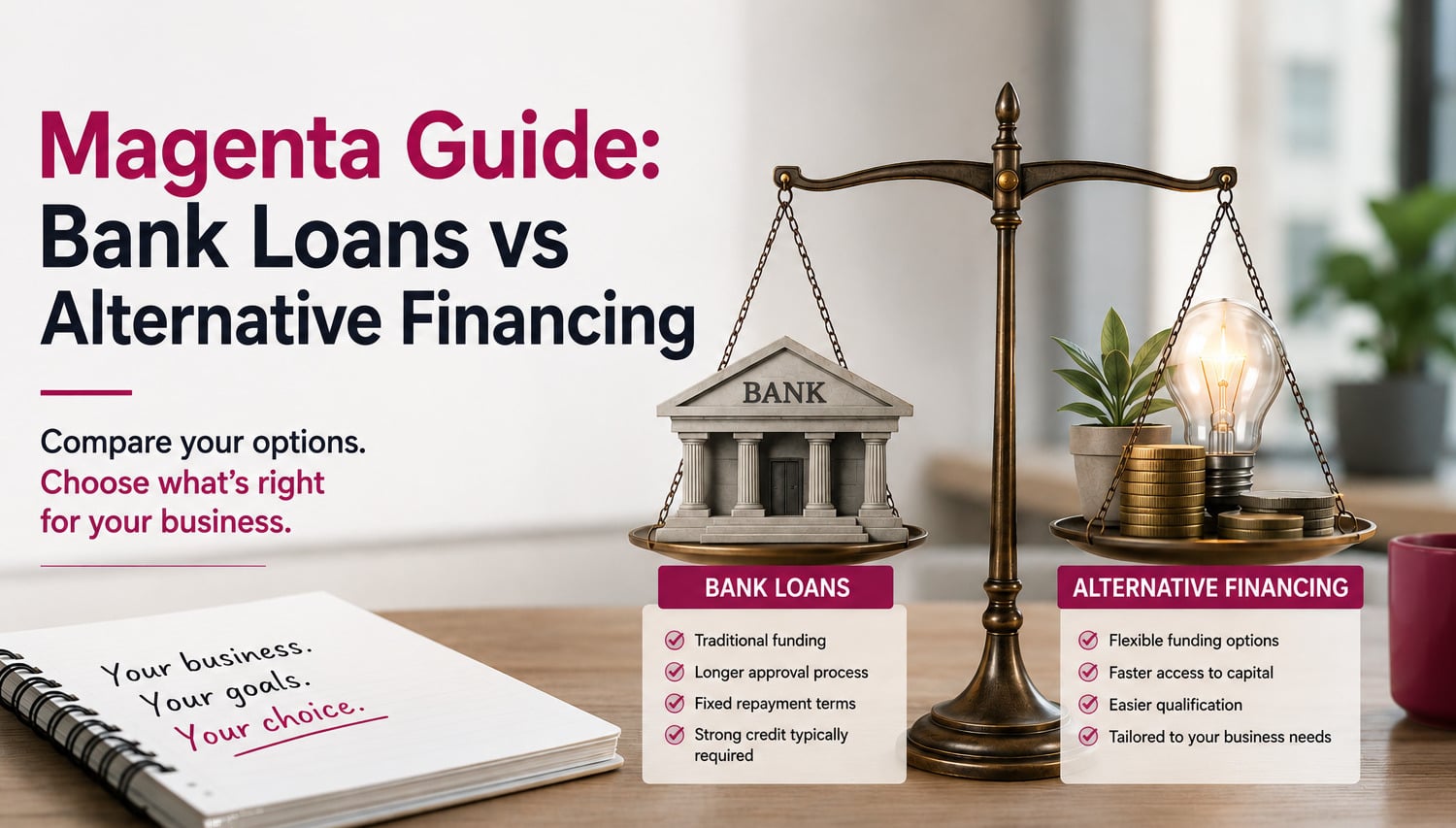

Magenta Guide: Bank Loans vs Alternative Financing