Magenta Guide: Bank Loans vs Alternative Financing

By Magenta on May 08, 2026

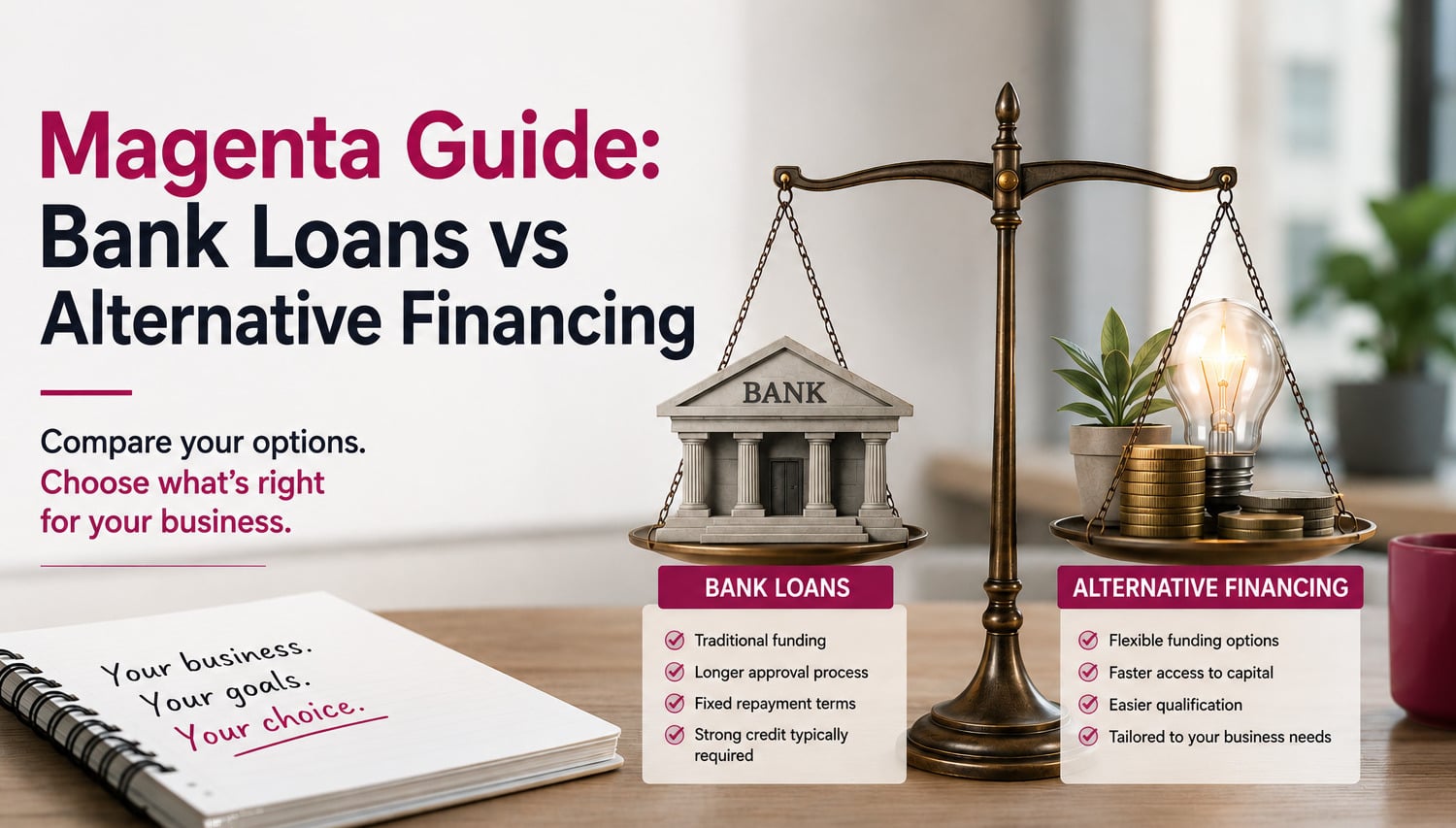

When your business needs capital, the first thought is often "get a bank loan." But for many small businesses, traditional bank financing isn't accessible — or fast enough. That's where alternative financing options like revenue-based financing come in.

Let's compare both paths so you can make the right choice for your business.

How Bank Loans Work for Small Businesses

Most small business owners start their funding journey at the same place: the bank. Traditional bank loans are structured forms of financing where a business borrows a fixed amount and repays it over a set term with interest. The process usually begins with an application that includes business financials, tax returns, and a personal credit check.

Timeline from application to funding: On average, according to the SBA.gov and Federal Reserve data, it takes 33 to 45 days for approval and funding to be completed. That timeline can stretch longer if collateral is required or if the business is new.

A typical journey includes:

- Application submission

- Credit and collateral review

- Underwriting decision

- Approval and closing

- Funding release

Takeaway: Bank loans remain a valuable option for established businesses with strong financial histories. However, they often move slowly and favor lower-risk applicants. If you need funding quickly or have inconsistent revenue, a bank loan may not be the right fit.

The Pros and Cons of Bank Loans

Every funding choice has trade-offs. Bank loans can offer stability, but not every small business qualifies. According to the 2025 Federal Reserve Small Business Credit Survey, only 47% of small businesses received the full amount they requested from banks.

When banks deny applications, it's often due to limited operating history or fluctuating cash flow. As industry experts note, banks prioritize consistency, businesses with variable revenue streams often struggle to fit that model.

Takeaway: Bank loans work best for established businesses with stable revenue, strong credit, and assets to pledge. If your business is newer, seasonal, or has variable income, you'll likely face challenges getting approved — or waiting weeks for a decision.

What Is Alternative Financing?

Alternative financing refers to funding options outside of traditional banks. These include online finance providers, peer-to-peer (P2P) platforms, merchant cash advances (MCAs), and revenue-based financing (RBF). Each comes with unique structures and benefits.

According to Fundera, alternative financing now represents 40% of all small business funding sources in the U.S., signaling a major shift toward flexibility and speed.

Takeaway: Alternative financing has grown rapidly because it solves problems traditional banks can't — speed, flexibility, and accessibility for businesses that don't fit the traditional mold. Revenue-based financing, in particular, offers a sustainable middle ground between expensive MCAs and slow bank processes.

Revenue-Based Financing: The Modern Alternative

Here's the key: Revenue-Based Financing is not a loan. It's a purchase agreement — the funder purchases a portion of future revenue until the agreed amount is delivered. No fixed terms, no interest rate, and no collateral.

How it works:

- You receive funds with approval focused on your business's performance, not your personal credit score

- Funding available up to $250K

- Your payment is set at approval and does not increase as your revenue grows, giving you a consistent structure you can plan around

- If revenue slows, you can request a review a temporary adjustment may be approved, with no penalties or fees

Legally, RBF differs from a loan because it's tied to performance, not debt.

Why Revenue-Based Financing is different from Merchant Cash advances:

While both are tied to revenue, MCAs typically require fixed daily or weekly withdrawals, regardless of revenue fluctuations, with a set total payback. RBF is structured around monthly performance, with adjustments available upon request during slower periods

Takeaway: Revenue-based financing offers the speed of alternative financing with a structure designed for sustainable growth. Unlike MCAs, if revenue slows you can request a review and a temporary adjustment may be approved - so slow months don't create cash flow emergencies.

Curious if revenue-based financing fits your business? Use Magenta's free Funding Calculator to see what you might qualify for — no commitment, no credit check.

Bank Loans vs Alternative Financing: Direct Comparison

Below is a side-by-side look at traditional bank loans versus modern financing options such as RBF.

Takeaway: Bank loans offer lower costs but higher barriers and slower timelines. Revenue-based financing offers speed and flexibility with approval focused on business performance, not personal credit score. The right choice depends on your business's situation, timeline, and cash flow patterns.

When to Choose a Bank Loan

Let's imagine Jane, a bakery owner with three years of steady revenue. Her sales are consistent month-to-month, and she's ready to open a second location. Because of her track record and profitability, a bank loan might be a fit — she can handle fixed monthly payments and benefit from a lower rate.

Bank loans make sense when:

- You have strong credit (680+) and stable revenue

- You need larger, long-term funding for major investments

- You're comfortable with collateral-backed commitments

- You can wait 4 – 6 weeks for approval and funding

- Your business has 2+ years of consistent financial history

As experts at the National Small Business Association advise, established businesses with predictable income and assets to pledge often gain the most from traditional financing.

Takeaway: If you have strong credit, stable revenue, time to wait, and collateral to offer, a bank loan may provide the lowest-cost funding option. But if any of those elements are missing, you'll likely face rejection or delays.

When to Choose Alternative Financing

Now meet Mark, who runs a seasonal landscaping business in Florida. His revenue peaks in summer but dips significantly in winter. Traditional bank financing doesn't fit his cash flow — fixed monthly payments would strain his business during slow months.

That's where revenue-based financing shines.

Alternative financing works best for:

- Businesses with variable or seasonal income

- Owners who need fast access to capital (days, not weeks)

- Companies seeking a payment structure with flexibility available upon request

- Business owners with limited or imperfect credit history

- Situations where collateral isn't available or desirable

Community feedback from forums like Reddit's small business shows growing support for RBF options, especially among business owners frustrated by long bank timelines and rigid payment structures.

Takeaway: If your revenue fluctuates, you need funding quickly, or you don't qualify for traditional bank financing, revenue-based financing offers a practical path forward with a payment structure designed to work with your business, not against it.

Why Magenta Is a Loan Alternative

Magenta is an alternative finance provider that helps businesses receive funding based on performance — not credit scores. With offers typically within an hour and next-day funding available, it's designed for business owners who need agility without sacrificing transparency.

How Magenta Works:

- Apply in minutes at magentafunding.com/apply

- Receive an offer — typically within an hour

- Get funded — as soon as the next business day

What you get with Magenta:

Why business owners choose Magenta:

- Speed without sacrifice — Fast as MCAs, but without aggressive daily deductions

- Payments that make sense — a defined structure with adjustments available upon request

- A partner, not just a provider — Every client works with a dedicated funding advisor

- No minimum credit score — approval focused on your business's revenue and performance

- Transparency from day one — No confusing terms or hidden fees

It's the modern answer to traditional bank financing: structured, fast, and transparent.

Takeaway: Magenta bridges the gap between slow bank processes and expensive MCAs offering fast funding with a defined payment structure and transparent terms. It's designed for businesses that need capital to grow without the stress of rigid repayment structures.

Wondering how much funding your business could access? Get a quick estimate based on your revenue. No paperwork, no obligation. See Your Options

Common Myths About Alternative Financing

Myth 1: Only businesses with bad credit use RBF

Not true. Many high-performing companies use RBF to maintain cash flow flexibility. Unlike traditional financing, RBF doesn't penalize you for short-term revenue dips; adjustments can be requested if revenue slows.

Myth 2: RBF is the same as a Merchant Cash Advance

They may look similar, but RBF is structured differently. MCAs typically involve daily deductions from card sales with a fixed total repayment. RBF payments are tied to monthly revenue performance, with adjustments available upon request. The cash flow impact is significantly different.

Myth 3: Alternative financing is always expensive

Costs depend on your specific situation and revenue performance. With RBF, if revenue slows, you can request a review — a temporary adjustment may be approved, protecting your cash flow. The flexibility often outweighs the cost difference compared to rigid bank financing that doesn't adapt to your business reality.

Myth 4: You need perfect credit for any business funding

Traditional banks often require credit scores of 680+. But alternative finance providers like Magenta focus on business performance — revenue, consistency, and trajectory — not personal credit history. Many successful funding relationships start with business owners who were turned down by banks.

Takeaway: Don't let myths about alternative financing prevent you from exploring options that might fit your business better than traditional banks. RBF is used by growing businesses of all credit profiles, and it's structurally different from MCAs in ways that matter for your daily cash flow.

Ready to skip the 6-week wait? Magenta delivers offers within an hour and funding as soon as the next business day. See if revenue-based financing is right for you. Get Started.

Choosing the Right Path for Your Business

Before deciding, ask yourself these five questions:

If you answered "RBF" to most questions, revenue-based financing could be the better fit for your business.

Takeaway: There's no one-size-fits-all answer. The right funding choice depends on your revenue patterns, timeline, credit situation, and comfort with fixed vs. flexible payments. Be honest about your business's reality when making the decision.

Conclusion: Finding the Right Funding Fit

Choosing between bank loans and alternative financing isn't about which is "better" — it's about which is better for your business right now.

Bank loans offer lower costs and predictability, but they require strong credit, collateral, stable revenue, and patience. Many small businesses — especially newer ones, seasonal operations, or those with variable income - simply don't qualify or can't wait weeks for funding.

Revenue-based financing offers a modern alternative: fast access to capital with a defined payment structure and flexibility available upon request. No minimum credit score, no collateral, and funding as soon as the next business day.

For business owners caught between slow bank processes and expensive MCAs, Magenta's revenue-based financing provides a balanced solution combining speed with structure, and accessibility with transparency.

The bottom line: Your funding should work with your business, not against it. Whether that's a traditional bank loan or revenue-based financing depends on your unique situation, but now you have the information to make the right choice.

Ready to Explore Your Options?

If you're tired of waiting weeks for bank decisions — or worried about the cash flow impact of rigid repayment structures — Magenta's revenue-based financing might be the solution you've been looking for.

Here's how to get started:

→ Option 1: Check your eligibility in minutes Use Magenta's Funding Calculator to see what you might qualify for based on your business revenue. No commitment, no credit check, just a quick estimate to help you plan.

→ Option 2: Talk to a funding advisor Have questions? Want to understand how revenue-based financing would work for your specific situation? Connect with a dedicated Magenta funding advisor who can walk you through your options.

→ Option 3: Apply now Ready to move forward? Start your application most businesses receive offers within an hour, with funding available as soon as the next business day.

Invest in possible.

FAQs

Yes. A previous bank denial doesn't disqualify you from alternative financing. Alternative finance providers like Magenta evaluate your business differently, approval is focused on revenue and business performance, not the credit criteria that typically lead to a bank rejection. If your business generates consistent revenue, you may still qualify.

It depends on your situation. Bank loans typically have lower rates but require strong credit, collateral, and longer timelines. Revenue-based financing offers flexibility that bank loans don't and for many businesses, that flexibility is worth the difference.

Magenta typically provides offers within an hour and can be funded as soon as the next business day compared to 4 - 6 weeks for most bank loans.

Magenta doesn't require a hard credit pull for initial eligibility. Approval is focused on your business's revenue and performance, not your personal credit history.

Both are tied to revenue, but MCAs typically require daily deductions from card sales with a fixed total repayment. With RBF, if revenue slows, you can request a review and a temporary adjustment may be approved providing more breathing room than MCAs during slow periods.

Subscribe by email

These Related Insights

Merchant Cash Advances vs Revenue-Based Financing: Which Is Better for Your Business?

The Benefits of Revenue-Based Financing for Small Businesses